Introduction

Every asset eventually reaches the end of its useful life. Whether it’s a company vehicle, a manufacturing machine, or a computer system, there comes a point when the asset is no longer useful for business operations. But even then, the asset may still hold some monetary worth. That remaining worth is known as salvage value.

Understanding salvage value is essential in accounting, finance, and asset management. It helps businesses estimate depreciation, determine resale potential, and make smarter financial decisions regarding equipment, property, and technology investments.

In reality, the concept influences everything from corporate balance sheets to small-business bookkeeping. If a business fails to estimate this value correctly, financial statements can become inaccurate, affecting profitability analysis and tax calculations.

This guide explains the meaning, formula, and practical uses of salvage value with real-world examples and easy explanations.

What Is Salvage Value

4

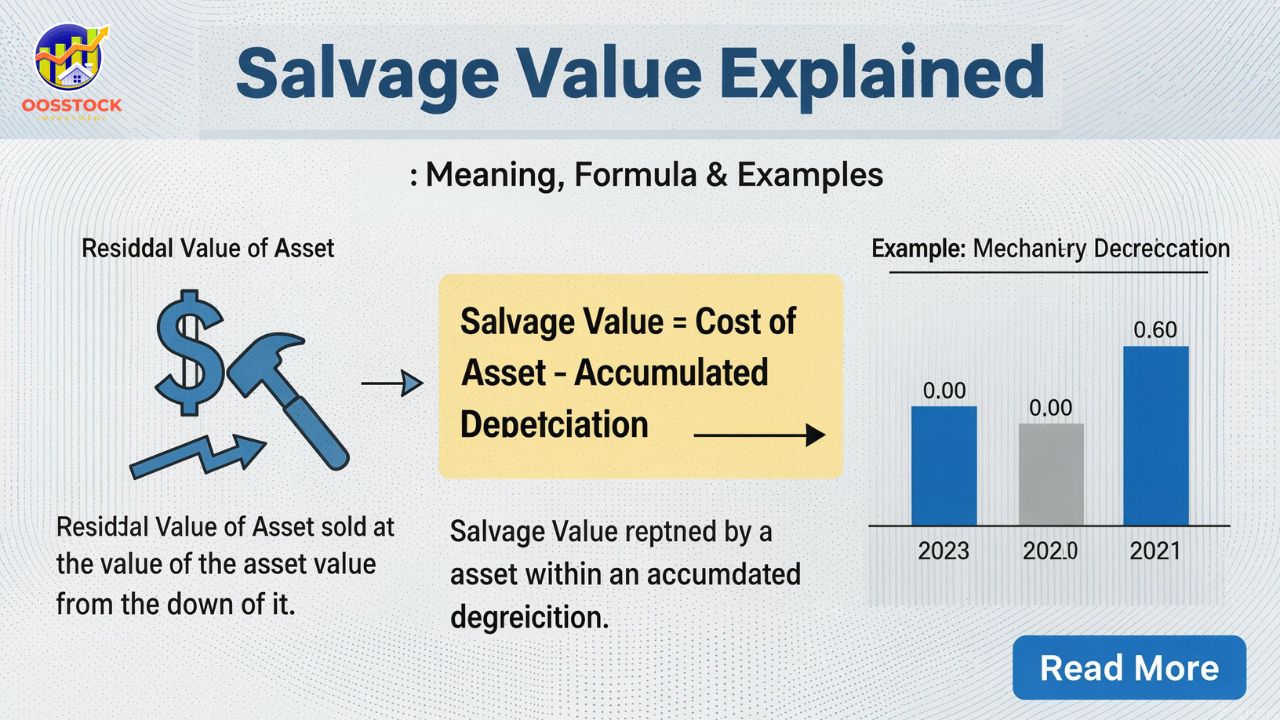

Salvage value refers to the estimated amount a company expects to receive when an asset reaches the end of its useful life and is sold, recycled, or scrapped.

In accounting terms, it represents the remaining value of an asset after all depreciation expenses have been recorded.

For example:

| Asset | Purchase Price | Useful Life | Estimated Salvage Value |

|---|---|---|---|

| Delivery Truck | $40,000 | 8 years | $5,000 |

| Office Computer | $2,000 | 4 years | $200 |

| Manufacturing Machine | $120,000 | 10 years | $15,000 |

Once the useful life ends, the business expects to recover the salvage amount by selling or recycling the asset.

Simple Definition

Salvage value is:

The estimated resale or scrap value of an asset at the end of its useful life.

Other Names for Salvage Value

You might hear this concept referred to as:

- Residual value

- Scrap value

- Disposal value

- Asset recovery value

Each term describes the remaining monetary worth of an asset after depreciation.

Why Salvage Value Matters in Accounting

4

For businesses, estimating salvage value correctly is extremely important because it directly affects depreciation calculations.

Depreciation determines how the cost of an asset is spread over its useful life.

Key Reasons It Matters

1. Accurate Financial Statements

If salvage value is overestimated or underestimated, depreciation expenses become incorrect. This can distort:

- Profit calculations

- Balance sheet values

- Asset reporting

2. Tax Calculations

Many tax authorities allow depreciation deductions. If the salvage value is wrong, companies may claim incorrect tax deductions.

3. Asset Replacement Planning

Companies use salvage estimates to decide when to replace equipment.

For example:

A logistics company may replace trucks after 7 years because the resale value drops significantly afterward.

4. Budget Forecasting

Knowing potential resale values helps businesses estimate future cash flows.

Salvage Value in Depreciation Calculations

One of the most important uses of salvage value is in depreciation formulas.

When businesses calculate depreciation, they subtract salvage value from the asset’s original cost.

Depreciable Amount Formula

| Component | Formula |

|---|---|

| Depreciable Cost | Asset Cost – Salvage Value |

Example:

Asset Cost = $50,000

Salvage Value = $5,000

Depreciable Amount:

$50,000 – $5,000 = $45,000

That $45,000 is the amount that will be depreciated over the asset’s useful life.

How to Calculate Salvage Value

Unlike depreciation formulas, there is no universal formula for determining salvage value. Instead, businesses estimate it based on experience, industry data, and market trends.

Common Estimation Methods

1. Market Comparison

Businesses analyze resale prices for similar used assets.

Example:

A 5-year-old forklift might sell for 15% of its original value.

2. Scrap Value Method

Some equipment has value only as scrap materials.

For example:

- Metal machinery

- Vehicles

- Construction equipment

The salvage value equals scrap metal value.

3. Percentage Method

Many companies use a fixed percentage of the purchase price.

Typical estimates:

| Asset Type | Typical Salvage % |

|---|---|

| Vehicles | 10–20% |

| Computers | 5–10% |

| Heavy Machinery | 15–25% |

| Furniture | 5–15% |

4. Professional Appraisal

Large companies often hire valuation experts to estimate asset resale value.

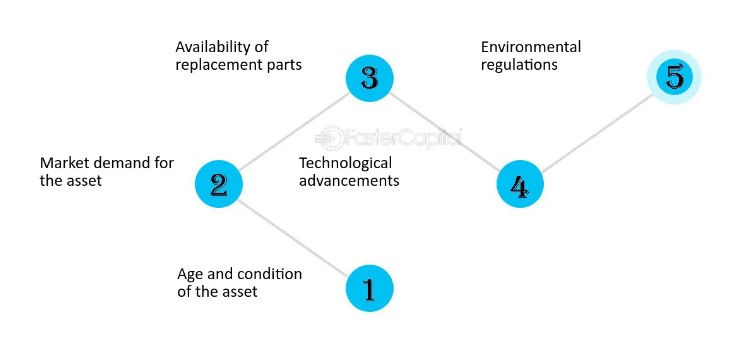

Factors That Affect Salvage Value

Many variables influence the final salvage amount an asset may have.

1. Asset Condition

The better the maintenance, the higher the resale value.

2. Market Demand

Technology equipment loses value faster because newer versions replace older models.

3. Technological Obsolescence

Rapid innovation lowers resale prices.

For example:

Smartphones lose value much faster than industrial equipment.

4. Maintenance History

Assets with documented maintenance records often retain higher value.

5. Economic Conditions

During economic downturns, second-hand equipment prices may drop

Salvage Value vs Residual Value

Although often used interchangeably, there is a slight difference between these two terms.

| Feature | Salvage Value | Residual Value |

|---|---|---|

| Common Use | Accounting | Leasing & finance |

| Meaning | Asset value at end of useful life | Estimated value at lease end |

| Context | Depreciation calculations | Lease agreements |

In practice, many businesses treat the two terms similarly.

Real-Life Examples of Salvage Value

Understanding real situations helps make the concept clearer.

Example 1: Delivery Van

A company purchases a delivery van for $30,000.

Expected useful life: 6 years

Estimated salvage value: $4,000

Depreciable cost:

$30,000 – $4,000 = $26,000

Annual depreciation:

$26,000 ÷ 6 = $4,333

Example 2: Office Computers

A startup buys computers worth $10,000.

After four years, the machines may only be sold for $1,000 total.

Thus:

Salvage value = $1,000

Example 3: Factory Machinery

Industrial machines often retain strong resale value.

Purchase price: $200,000

Estimated salvage value: $25,000

Depreciable cost:

$175,000

Salvage Value in Different Depreciation Methods

Different accounting methods treat depreciation differently, but salvage value remains a critical component.

Straight-Line Depreciation

Most common method.

Formula:

Annual Depreciation =

(Asset Cost – Salvage Value) ÷ Useful Life

Declining Balance Method

Faster depreciation during early years.

Salvage value acts as a minimum asset value threshold.

Units of Production Method

Used for machinery and production equipment.

Depreciation is based on usage rather than time.

Example:

Machine expected output: 100,000 units.

Depreciation per unit:

(Asset Cost – Salvage Value) ÷ Total Units

Accounting Standards and Salvage Value

International accounting standards require businesses to review asset estimates periodically.

IFRS Requirements

Under International Financial Reporting Standards:

Companies must review salvage estimates at least once per year.

If the estimate changes, depreciation schedules must be updated.

GAAP Requirements

Under U.S. Generally Accepted Accounting Principles:

Companies must estimate salvage value when assets are initially recorded.

Changes must be documented and disclosed.

Common Mistakes When Estimating Salvage Value

Businesses often make errors when estimating this value.

1. Setting Salvage Value Too High

This reduces depreciation expense and artificially increases profits.

2. Ignoring Market Trends

Technology assets depreciate faster than expected.

3. Never Updating Estimates

Asset markets change over time.

4. Using Guesswork Instead of Data

Professional appraisals and market research provide better estimates.

FA

What is salvage value in accounting?

Salvage value is the estimated amount a company expects to receive when selling or disposing of an asset after its useful life ends.

Is salvage value always positive?

Not always. Some assets may have zero salvage value if disposal costs equal resale value.

Can salvage value change?

Yes. Businesses may revise salvage estimates based on market changes or asset condition.

Is salvage value used for tax depreciation?

Many tax systems require depreciation calculations, though rules may differ from accounting standards.

What happens if salvage value is incorrect?

Incorrect estimates lead to inaccurate depreciation expenses and financial statements.

Is salvage value the same as scrap value?

Scrap value is a type of salvage value, usually referring to the value of materials after dismantling an asset.

Why do accountants subtract salvage value from asset cost

Because depreciation only applies to the portion of an asset that will lose value during its useful life.

Do all assets have salvage value?

No. Some assets become obsolete and have no resale value.

Conclusion

Understanding salvage value is essential for accurate financial reporting, smart asset management, and effective business planning. By estimating the remaining value of an asset at the end of its useful life, companies can calculate depreciation properly and maintain reliable financial records.

While the concept may seem simple, its impact reaches across accounting, taxation, and investment decisions. Businesses that regularly review asset values, monitor market trends, and maintain equipment carefully can maximize their asset recovery while keeping financial statements accurate.

In a world where equipment, technology, and infrastructure represent major investments, understanding salvage value helps companies protect their financial health and make better long-term decisions.