Introduction

Imagine two companies generating the same revenue. One achieves it using minimal resources, while the other requires massive investments in equipment, buildings, and inventory. Which one is more efficient? That’s where the asset turnover ratio becomes incredibly valuable.

The asset turnover ratio reveals how effectively a company uses its assets to produce sales. Investors, analysts, and business owners rely on this metric to understand whether assets are working hard—or sitting idle.

In reality, many businesses struggle not because they lack assets, but because they fail to use them efficiently. A warehouse full of equipment, vehicles, or machinery means little if those assets are not generating meaningful revenue.

Understanding this ratio can transform how you evaluate business performance. Whether you’re an investor comparing companies, an entrepreneur improving operations, or a finance student learning financial analysis, this metric offers deep insights into operational efficiency.

What Is Asset Turnover Ratio

The asset turnover ratio measures how efficiently a company uses its assets to generate revenue.

Simply put, it answers one key question:

“How much sales revenue does a company generate for every dollar of assets it owns?”

If a company has a high ratio, it means the business uses its resources efficiently. If the ratio is low, assets might be underutilized.

Basic Definition

Asset turnover ratio =

Revenue generated ÷ Total assets

The ratio reflects operational efficiency rather than profitability.

A company can have high profits but still operate inefficiently if its assets are not producing enough sales.

Why It Matters

Businesses invest heavily in assets like:

- Equipment

- Buildings

- Vehicles

- Technology infrastructure

- Inventory

If these assets do not produce adequate revenue, capital becomes trapped, reducing overall efficiency.

Asset Turnover Ratio Formula Explained

Understanding the formula helps clarify how the ratio works.

Standard Formula

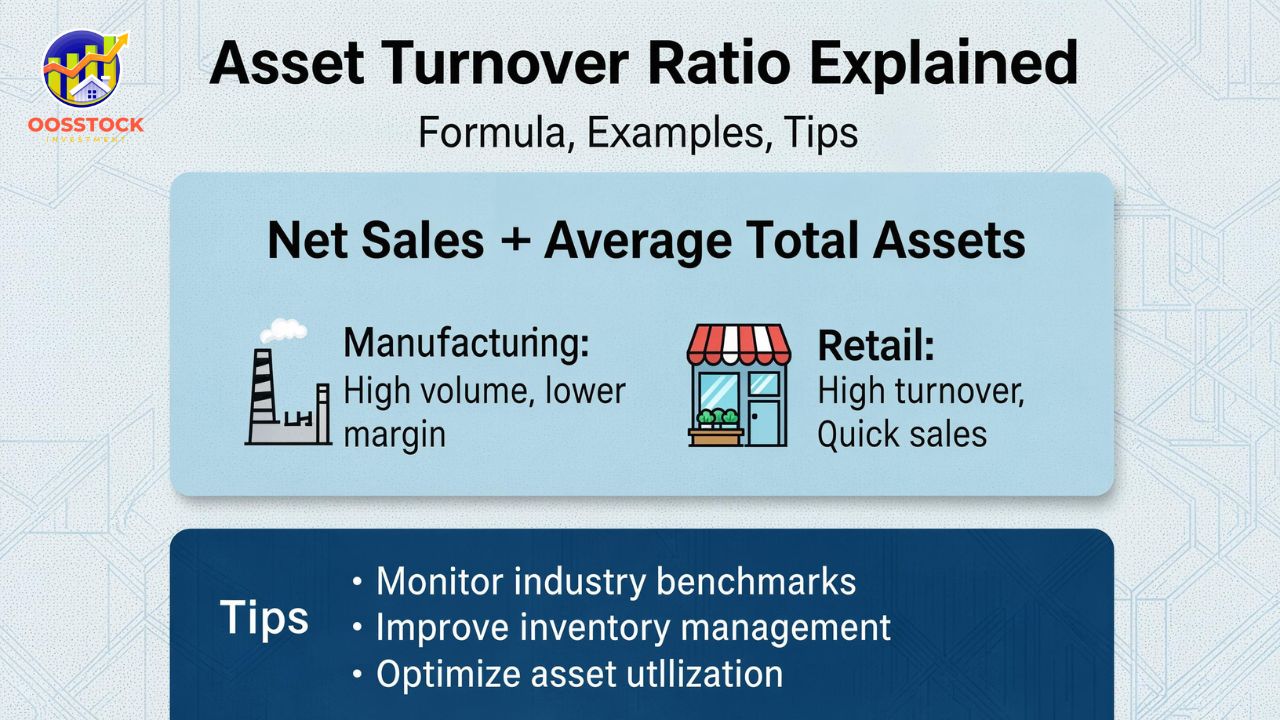

Asset Turnover Ratio = Net Sales / Average Total Assets

Where:

Net Sales

Total revenue generated from operations after returns and allowances.

Average Total Assets

Average of assets at the beginning and end of the accounting period.

Expanded Formula

Average Total Assets =

(Beginning Assets + Ending Assets) / 2

Using the average prevents distortion caused by sudden asset purchases or disposals during the year.

How to Calculate Asset Turnover Ratio

Let’s walk through a practical example.

Example

A company reports:

- Net Sales: $2,000,000

- Beginning Assets: $800,000

- Ending Assets: $1,200,000

First calculate average assets.

Average Assets =

(800,000 + 1,200,000) / 2 = 1,000,000

Now calculate the <strong>asset turnover ratio</strong>.

Asset Turnover Ratio =

2,000,000 / 1,000,000 = 2.0

Interpretation

This means the company generates $2 of sales for every $1 of assets.

That is generally considered efficient, though the ideal ratio varies by industry.

Real-Life Examples of Asset Turnover Ratio

Different companies demonstrate how this metric varies widely across industries.

Example 1: Retail Company

Retail businesses typically have high ratios because they rely on inventory turnover.

Example:

| Metric | Value |

|---|---|

| Net Sales | $5,000,000 |

| Average Assets | $1,500,000 |

| Ratio | 3.33 |

Retail companies often achieve ratios above 2.5.

Example 2: Manufacturing Company

Manufacturers invest heavily in machinery and factories.

| Metric | Value |

|---|---|

| Net Sales | $10,000,000 |

| Average Assets | $8,000,000 |

| Ratio | 1.25 |

This is normal because capital investment is high.

Example 3: Technology Company

Tech companies rely more on intellectual property than physical assets.

| Metric | Value |

|---|---|

| Net Sales | $20,000,000 |

| Average Assets | $6,000,000 |

| Ratio | 3.33 |

Asset-light business models tend to show higher efficiency.

Why Asset Turnover Ratio Matters for Businesses

Companies operate in competitive environments where efficiency determines survival.

A healthy asset turnover ratio indicates a company is maximizing resources.

Benefits of a High Ratio

- Efficient use of capital

- Strong operational performance

- Better return on investments

- Improved investor confidence

Operational Insights

Managers can use the ratio to evaluate:

- equipment productivity

- inventory utilization

- logistics efficiency

- asset allocation decisions

If assets are not generating sufficient revenue, businesses must reconsider their strategy.

Interpreting Asset Turnover Ratio

Numbers alone mean little without context.

The asset turnover ratio must always be interpreted relative to:

- industry averages

- company history

- competitors

- business model

General Interpretation Guide

| Ratio | Meaning |

|---|---|

| Above 2.5 | Highly efficient |

| 1.5 – 2.5 | Strong performance |

| 1.0 – 1.5 | Moderate efficiency |

| Below 1.0 | Poor asset utilization |

However, these ranges vary significantly across industries.

High vs Low Asset Turnover Ratio

Understanding what drives high or low ratios helps improve business performance.

High Ratio Characteristics

Companies with high efficiency usually:

- operate asset-light models

- have strong inventory turnover

- maintain lean operations

- focus on high-volume sales

Examples include:

- supermarkets

- online marketplaces

- fast-fashion retailers

Low Ratio Characteristics

Low ratios may indicate:

- expensive machinery

- underused equipment

- excess inventory

- poor management decisions

However, in capital-intensive sectors like airlines or utilities, lower ratios are expected.

Industry Differences in Asset Turnover Ratio

Different sectors naturally produce different ratios.

Typical Industry Benchmarks

| Industry | Average Ratio |

|---|---|

| Retail | 2.0 – 3.5 |

| Technology | 1.5 – 3.0 |

| Manufacturing | 1.0 – 2.0 |

| Telecommunications | 0.5 – 1.0 |

| Utilities | 0.3 – 0.7 |

These differences highlight why comparisons should always occur within the same industry.

How Businesses Can Improve Asset Turnover Ratio

Improving efficiency requires strategic decisions across operations.

1. Increase Revenue Without Increasing Assets

Companies can improve efficiency by generating more sales from existing resources.

Examples include:

- marketing improvements

- better pricing strategies

- expanding customer reach

2. Sell Underutilized Assets

Idle assets drain capital.

Businesses can:

- sell unused equipment

- lease instead of owning

- reduce excess inventory

3. Improve Inventory Management

Inventory often represents a large portion of assets.

Techniques include:

- just-in-time inventory

- demand forecasting

- faster product cycles

4. Optimize Asset Allocation

Companies must continuously review how assets are deployed.

For example:

A delivery company might improve route planning to ensure trucks operate at full capacity.

Limitations of Asset Turnover Ratio

Despite its usefulness, the asset turnover ratio has limitations.

Accounting Differences

Different accounting policies may distort asset values.

For example:

- depreciation methods

- asset revaluation

- leasing vs owning

Industry Comparisons

Comparing companies from different sectors can be misleading.

A manufacturing firm will always appear less efficient than a digital company.

Asset Age

Older assets that are heavily depreciated can artificially increase the ratio.

That may make the company appear more efficient than it actually is.

Asset Turnover Ratio vs Other Financial Ratios

Financial analysis requires examining multiple metrics.

Asset Turnover vs Return on Assets

| Metric | Focus |

|---|---|

| Asset Turnover | Efficiency of asset use |

| Return on Assets | Profit generated from assets |

A company may have a high ratio but still be unprofitable if margins are low.

Asset Turnover vs Inventory Turnover

Inventory turnover focuses specifically on stock management.

Asset turnover covers all company assets.

Asset Turnover vs Fixed Asset Turnover

Fixed asset turnover analyzes only long-term assets such as machinery and buildings.

This ratio is useful for capital-intensive businesses.

Practical Use in Investment Analysis

Investors frequently use asset turnover ratio when comparing companies.

The metric helps identify businesses that generate more revenue from fewer resources.

Investors Look For

- rising ratio over time

- higher ratio than competitors

- stable operational efficiency

Example Investment Insight

Two companies generate $10 million in revenue.

Company A assets = $5 million

Company B assets = $12 million

Company A ratio = 2.0

Company B ratio = 0.83

Investors typically prefer Company A because it uses assets more efficiently.

FAQ

What does asset turnover ratio indicate?

The asset turnover ratio indicates how efficiently a company uses its assets to generate sales revenue. A higher ratio means better efficiency.

What is a good asset turnover ratio?

A good ratio depends on the industry. Retail businesses often exceed 2.5, while utilities may operate below 1.0 due to heavy infrastructure investments.

How often should asset turnover ratio be calculated?

Most companies calculate it annually or quarterly when reviewing financial statements.

Is a higher asset turnover ratio always better?

Generally yes, but extremely high ratios may indicate insufficient asset investment, which could limit future growth.

What causes a low asset turnover ratio?

Low ratios can result from excess inventory, idle equipment, poor sales performance, or heavy capital investments.

How does depreciation affect asset turnover ratio?

Depreciation reduces asset values over time, which can increase the ratio even if operational efficiency does not improve.

Can startups have high asset turnover ratios?

Yes. Many startups operate with minimal physical assets, which can produce higher ratios.

Why do investors analyze asset turnover ratio?

Investors use it to identify efficient companies that maximize revenue using limited resources.

Conclusion

Understanding the asset turnover ratio provides valuable insight into how effectively a business converts assets into revenue. While profitability metrics often dominate financial discussions, efficiency metrics like this ratio reveal how well a company manages its resources.

Companies with strong operational discipline tend to generate more sales with fewer assets, creating a competitive advantage in crowded markets. At the same time, investors use this ratio to identify businesses that maximize capital efficiency.

However, no single metric tells the entire story. Asset turnover ratio should always be analyzed alongside profitability ratios, industry benchmarks, and long-term business strategies.

When used correctly, it becomes a powerful tool for evaluating performance, improving operations, and making smarter investment decisions.