Introduction

When analyzing a company’s financial health, one question matters more than most: can the business comfortably pay its debts? That’s exactly where the times interest earned ratio becomes incredibly useful.

The times interest earned ratio helps investors, analysts, and business owners understand how easily a company can cover its interest payments using its operating profits. In simple terms, it tells you whether a business earns enough money to stay ahead of its debt obligations.

Imagine lending money to a friend. Before handing over the cash, you’d want to know if they actually earn enough income to repay you. That’s essentially what lenders and investors are doing when they look at this ratio. It offers a quick snapshot of financial stability, debt management, and risk.

Understanding this metric can make a huge difference when evaluating investments, running a business, or studying finance. Let’s explore how it works, why it matters, and how to use it effectively.

What Is the Times Interest Earned Ratio

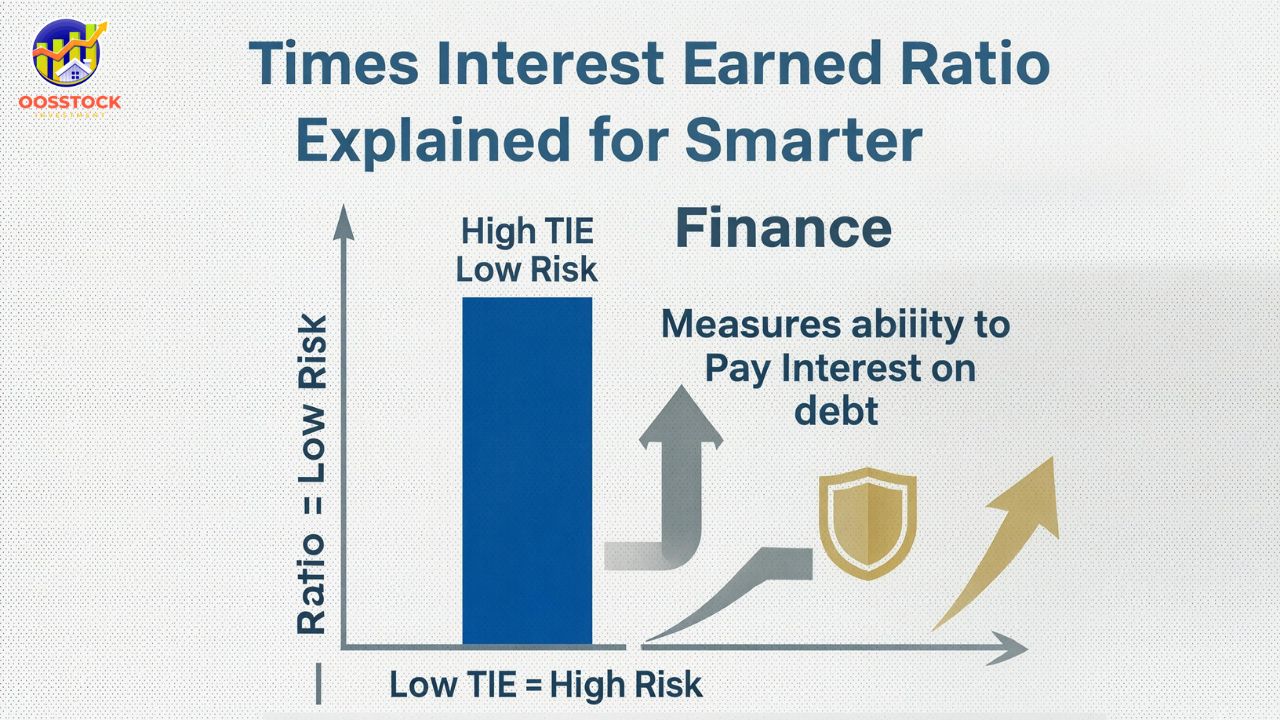

The times interest earned ratio is a financial metric used to determine how easily a company can pay interest expenses on its outstanding debt.

In essence, the ratio measures how many times a company’s operating profit can cover its interest obligations. The higher the number, the more comfortable the company is in paying its interest.

Financial analysts often refer to this metric as the interest coverage ratio. It is one of the most widely used solvency ratios in financial statement analysis.

Key Concept Behind the Ratio

At its core, the ratio answers a simple but powerful question:

How many times can a company’s earnings pay its interest bills?

For example:

- Ratio of 5 means profits can cover interest five times

- Ratio of 1.5 means profits barely cover interest

- Ratio below 1 signals financial trouble

This makes the metric incredibly useful for lenders evaluating credit risk and investors assessing long-term financial stability.

Why the Times Interest Earned Ratio Matters

Debt is a normal part of business. Companies borrow money to expand operations, invest in equipment, or fund new projects.

However, debt also creates risk.

If profits fall, interest payments still need to be made. This is where the times interest earned ratio becomes a crucial indicator.

Reasons This Ratio Is Important

- Measures financial safety

A high ratio indicates the company can comfortably pay its debts. - Helps lenders evaluate creditworthiness

Banks frequently examine this ratio before approving loans. - Signals financial distress early

A declining ratio may suggest growing financial risk. - Supports investment decisions

Investors often prefer companies with stable interest coverage. - Reveals debt management quality

It reflects how responsibly a company handles borrowing.

In many cases, a weak interest coverage ratio can be an early warning sign of potential financial trouble.

Formula for Calculating the Times Interest Earned Ratio

The calculation is relatively straightforward.

Standard Formula

Times Interest Earned Ratio =

EBIT ÷ Interest Expense

Where:

| Component | Meaning |

|---|---|

| EBIT | Earnings Before Interest and Taxes |

| Interest Expense | Total interest payable on debt |

EBIT represents the company’s operating earnings before financing costs and taxes are deducted.

Using EBIT ensures that we measure the company’s actual operating profitability when assessing its ability to pay interest.

How to Calculate the Ratio Step by Step

Calculating the times interest earned ratio involves a few simple steps using information from the income statement.

Step 1: Find EBIT

EBIT can usually be found on the income statement. If not listed directly, it can be calculated:

EBIT = Net Income + Interest Expense + Taxes

Step 2: Identify Interest Expense

Interest expense represents the total interest paid on loans, bonds, and other debt.

Step 3: Divide EBIT by Interest Expense

Once both numbers are known, divide EBIT by interest expense.

Example calculation:

| Item | Amount |

|---|---|

| EBIT | $500,000 |

| Interest Expense | $100,000 |

Times Interest Earned Ratio = 500,000 ÷ 100,000 = 5

This means the company earns five times the amount required to cover its interest payments.

Example of the Times Interest Earned Ratio in Real Life

Let’s look at a simple scenario.

Example: Manufacturing Company

A manufacturing company reports the following:

| Financial Item | Amount |

|---|---|

| Revenue | $4,000,000 |

| Operating Expenses | $3,200,000 |

| EBIT | $800,000 |

| Interest Expense | $200,000 |

Using the formula:

Times Interest Earned Ratio =

800,000 ÷ 200,000 = 4

This means the company can cover its interest payments four times.

Interpretation

- Ratio above 3 → usually considered safe

- Ratio between 1.5–2 → moderate risk

- Ratio below 1 → serious financial risk

The company in this example appears financially stable.

Interpreting the Times Interest Earned Ratio

Numbers alone don’t tell the full story. Context matters.

High Ratio

A high times interest earned ratio indicates:

- Strong profitability

- Low default risk

- Comfortable debt servicing

However, extremely high ratios could also mean the company is not leveraging debt effectively.

Moderate Ratio

A moderate ratio suggests:

- Stable but cautious financial health

- Reasonable debt management

Low Ratio

A low ratio signals potential problems:

- Weak profitability

- Difficulty covering interest

- Higher financial risk

Companies with ratios below 1.5 often face scrutiny from lenders.

What Is a Good Times Interest Earned Ratio

There is no universal “perfect” number. The ideal ratio varies across industries.

General Benchmarks

| Ratio | Meaning |

|---|---|

| Below 1 | Cannot cover interest payments |

| 1–2 | Risky financial position |

| 2–3 | Acceptable but cautious |

| 3–5 | Healthy coverage |

| Above 5 | Very strong financial stability |

Industry Differences

Industries with stable revenue streams often maintain higher ratios.

Examples:

- Utilities: high coverage ratios

- Technology: moderate ratios

- Manufacturing: varies depending on debt

Investors usually compare the ratio with industry averages rather than judging it in isolation.

Factors That Affect the Ratio

Several factors can influence the times interest earned ratio.

1. Profitability

Higher operating profits increase the ratio.

2. Debt Levels

More borrowing increases interest payments, lowering the ratio.

3. Economic Conditions

Economic downturns can reduce profits, shrinking coverage.

4. Interest Rates

Rising interest rates increase debt costs.

5. Business Cycles

Seasonal industries may experience fluctuating ratios.

Understanding these factors helps analysts interpret financial results more accurately.

Limitations of the Ratio

Despite its usefulness, the ratio is not perfect.

Major Limitations

- Ignores principal payments

The metric only considers interest, not loan repayments. - Depends on accounting methods

Different accounting practices can affect EBIT. - Does not measure cash flow directly

A company may have accounting profits but weak cash flow. - Industry variations matter

Comparing different industries may lead to misleading conclusions.

Because of these limitations, analysts typically combine it with other financial metrics.

How Investors and Lenders Use the Ratio

Financial professionals rely heavily on the times interest earned ratio when assessing companies.

Investors

Investors use the ratio to:

- Evaluate financial stability

- Compare companies within an industry

- Assess bankruptcy risk

- Identify sustainable earnings

Lenders

Banks and financial institutions use the ratio to:

- Determine loan approval

- Set borrowing limits

- Evaluate default risk

- Monitor financial health

For example, many banks require borrowers to maintain a minimum interest coverage ratio as part of loan agreements.

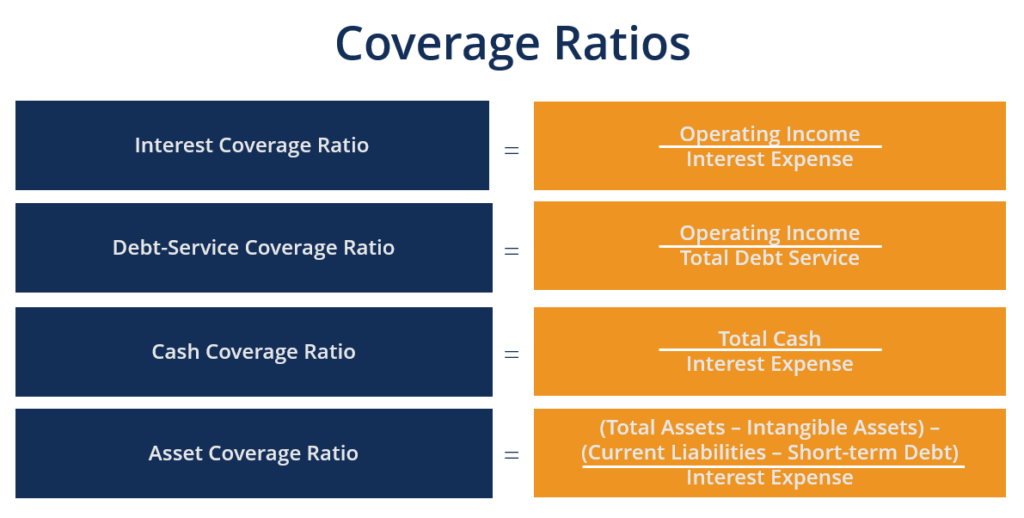

Comparing the Ratio with Other Financial Metrics

Financial ratios rarely stand alone. Analysts combine them with other indicators for a fuller picture.

Common Related Ratios

| Ratio | Purpose |

|---|---|

| Debt-to-Equity Ratio | Measures leverage |

| Current Ratio | Measures liquidity |

| Operating Margin | Measures profitability |

| Debt Service Coverage Ratio | Measures debt repayment ability |

The times interest earned ratio focuses specifically on interest coverage, while other metrics evaluate different aspects of financial health.

Improving a Company’s Interest Coverage

Companies can strengthen their ratio through several strategies.

Methods to Improve the Ratio

- Increase operating profits

- Reduce debt levels

- Refinance loans at lower interest rates

- Improve operational efficiency

- Cut unnecessary expenses

Better financial management can significantly improve interest coverage and reduce financial risk.

FAQ

What does the times interest earned ratio measure?

The times interest earned ratio measures how easily a company can pay its interest expenses using operating profits.

Why is the times interest earned ratio important?

It helps investors and lenders evaluate financial stability and determine whether a company can handle its debt obligations.

What happens if the ratio is below 1?

A ratio below 1 means the company does not generate enough earnings to cover interest payments.

Is a higher ratio always better?

Generally yes, but extremely high ratios may indicate that the company is not using debt efficiently.

What financial statement provides the data for this ratio?

The income statement provides EBIT and interest expense used to calculate the ratio.

Is the times interest earned ratio the same as interest coverage ratio?

Yes. Both terms are commonly used to describe the same financial metric.

How often should investors review this ratio?

Investors typically review it every quarter or annually when companies release financial statements.

Can startups have a low ratio?

Yes. Early-stage companies often have lower ratios because they invest heavily in growth.

Conclusion

The times interest earned ratio remains one of the most important financial metrics for evaluating a company’s ability to manage debt responsibly.

By showing how many times a business can cover its interest payments with operating profits, the ratio provides valuable insight into financial stability, risk exposure, and overall creditworthiness.

Investors, lenders, and business owners all rely on this metric when making financial decisions. While it should not be used alone, combining it with other financial ratios offers a powerful way to assess a company’s long-term financial health.

Understanding this ratio doesn’t just improve financial literacy—it can help you make smarter business and investment choices.